Alternative Assets in India: Immense scale or still a mirage?

Analysis of key numbers based on SEBI data.

A lot has been spoken about the the growth of alternative assets in India and how it has started to eclipse the traditional asset management business. Most of the alternative assets are managed by broadly two types of domestic regulatory structures i.e. AIF (Alternative Investment Fund) and PMS (Portfolio Management Service). While both the structures are mostly used for distinct investment strategies, they are also delineated by the threshold amounts for investors. In this article, I try to make sense of the data that is available for both the structures from the SEBI website.

1) Cumulative AIF Assets

AIFs have grown from managing commitments of INR 27,484crs (USD 3.7bn) to INR 4,05,118crs (USD 54.0bn) over a five year period ending Sept 2020. In terms of composition by asset class, Cat I AIFs (venture, infra funds) are about 10%, Cat III (hedge funds, public market vehicles) are 22% and Cat II (private equity et. al.) are the largest at 68% of the total. For those who are not familiar with categorization, please see notes to this article for detailed definitions.

It is pertinent to note that, the amounts of commitments raised and investments made vary significantly across categories but is broadly hovering at 41% on aggregate. Some of these differences may be on account of timing (venture and private equity funds raise commitments upfront but deploy capital over a 3–5 year period) and balance could be on account of deployment challenges (market conditions, ability to find good opportunities etc).

2 = Key Takeaways by Category

Infrastructure Funds have been laggards when it comes to growth in fresh commitments, but have seen investment activity go up. AUM for these funds now stands at INR 7,157crs (USD 1.0bn) with 60% of the total committed amount already invested.

Venture Capital Funds have shown an impressive commitment trajectory by growing from INR 1,631crs (USD 0.2bn) to INR 26,456crs (USD 3.5bn), but lag significantly behind in terms of investments made with only 32% of the capital deployed thus far. This could potentially be on account of most of the funds being raised in the 2017–2019 vintage. AUM for venture capital funds currently stands at INR 8,373crs (USD 1.1bn) as of Sept 2020.

As a part of the Covid19 relief package, Government of India had made a commitment of INR 50,000crs (USD 6.7bn) to funds targeting investments in SMEs through a fund-of-funds structure. While SME Funds have seen a recent uptick in terms of commitments, I expect it to materially go up in the next couple of years as more commitments and deployments are made by the Government.

Category III Funds are one of the most popular vehicles for public market and trading managers (long-short, long-only funds). These funds may also employ leverage for the purposes of their investments. Cat III funds have been one of the fastest growing categories and now form a sizeable chunk of the overall AIF asset class. Commitments have grown at CAGR of 74% from INR 3,516crs (USD 0.5bn) to INR 49,364crs (USD 6.6bn) and these funds also have the highest deployment rate at 75% partially due to nature of the business.

Cat III has been extremely popular product with HNI investors who are looking at exposure to public markets through specialized investment managers. On the flipside, there have been few hiccups in growth for Cat III due to the flux in the taxation regime for these funds.

So that leaves us with the last but the largest category — Category II Funds. As per the definition of SEBI, anything that does not fall in Category I or III is effectively Category II and additionally these funds are not allowed to take leverage for their investments.

Having said that, Cat II funds have been conspicuously used by domestic and global private equity funds to set up local investment vehicles. While Cat II allows them to pool investments locally, these funds also do not have the FDI restrictions that otherwise act as a hindrance for private equity investors in the regulated sectors (retail, insurance etc). Cat II Funds have grown from INR 14,707crs (USD 2.0bn) to INR 3,14,309crs (USD 41.9bn) in total commitments raised but current deployment hovers at only 36%. The contribution of Cat II vehicles to annual PE/VC flows in India is still miniscule. I had written a detailed note on PE/VC flows here.

Most of these funds raise monies from non-domestic, non-retail investors and hence necessarily do not reflect the migration towards alternatives from an Indian perspective.

So, if one were to just look at Cat I + Cat III as truly representing alternative assets for investors, then these two jointly are at about INR 90,809crs (USD 12.1bn) in commitments and INR 53,654crs (USD 7.2bn) in deployed investments. In terms of deployed capital, these two categories combined have grown at a CAGR of 65% and now account for 32% of total AIF investments.

3 = Portfolio Management Services

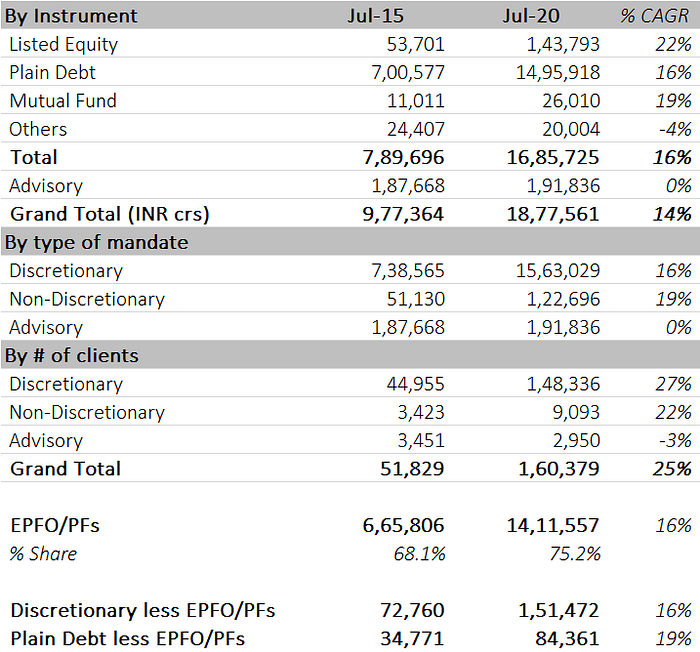

The overall AUM for portfolio managers stands at INR 18.7lac crs (USD 250bn) as of July 2020 and has grown at a CAGR of 14% over the last 5 years. However, the most significant contribution is from funds managed for EPFO/PFs which is 75% of the total AUM. Given the high contribution from the retirement funds, the portfolio looks skewed towards ‘Plain Debt’ when one looks at the data by instrument.

I would like to believe that the ‘Listed Equity’ category is by and large the true representative of the Alternative Assets here. This category has grown from INR 53,701crs (USD 7.2bn) to INR 1,43,793crs (USD 19.2bn) at CAGR of 22%. Infact in terms of number of clients, the Discretionary pool has grown the fastest at 27% in the last 5 years.

This movement to PMS has been partly driven by the challenges in the mutual fund industry which I wrote about here.

4 = Overall Picture

If you look at the relevant corpus between AIF and PMS, then the total relevant AUM (Cat I, Cat III from AIF and Listed Equity from PMS) is roughly at INR 1,97,447crs (USD 26.3bn). It is up from INR 58,119crs (USD 7.7bn) in 2015 thereby demonstrating a 5yr CAGR of 28%.

So once you separate the wheat from the chaff, the alternative assets industry looks much smaller in size but is still witnessing a very healthy growth trajectory.

To put Alternatives Assets’ size in perspective, the AUM of mutual fund industry stands at INR 29.8lac crs (USD 398bn), which means Alternative Assets are just 6.6% of the mutual fund industry. This implies that we certainly have a long road ahead for Alternative Assets in India.

Some of the drivers that could expedite the movement to Alternative Assets will include introduction of innovative products, better alignment of manager’s economics, appropriate benchmarking of returns, and full transparency in business practices.

Definitions:

AIF

Category I AIF: AIF which invest in start-ups or early stage ventures or social ventures or SMEs or infrastructure or other social sectors.

Category II AIF: AIF which do not fall in Category I and III and which do not undertake leverage or borrowing other than to meet day-to-day operational requirements.

Category III AIF: AIF which employ diverse or complex trading strategies and may employ leverage including through investment in listed or unlisted derivatives.

The taxation regime for each of the AIF categories is also different.

PMS

Discretionary PMS: The discretionary portfolio manager individually and independently manages the funds of each client in accordance with the needs of the client.

Non-discretionary PMS: The non-discretionary portfolio manager manages the funds in accordance with the directions of the client.

Notes:

All figures converted using a standard exchange rate of 1 USD=75 INR.